Injuries at work can result from negligence on your part as an employee or the employer’s failure to provide a safe working environment. Either way, you need to get compensation to support your recovery and possibly return to work when this happens.

Also, insurance companies will always investigate claims from policyholders to ensure that you file legitimate cases. It’s a precondition that most people overlook when enlisting the insurers’ services. So, you must read the underlying clauses in an insurance contract to avoid surprises, such as claims rejection by the insurer.

In particular, workers’ compensation covers work-related injuries from working hours or duties. They’re injuries that take longer to recover, and you may spend a fortune of up to $2000 per 10 day period to treat your ailment. The claims process is cumbersome due to the underlying law considerations; thus, consulting an insurance lawyer might be your best decision.

Are you wondering how you can get compensated for your work-related injuries? Below are eight steps to follow.

1.Inform Your Employer

The first cause of action is to report the matter to your employer and ensure it goes on company records. It helps to eliminate doubts about your injury at the workplace and contributes to the evidence needed to file your claims. It also adheres to workplace safety that requires employers to provide and maintain injury record books as a tool to improve the working environment.

Moreover, workers’ compensation claims might have a timeline of 30 days minimum for you to report to relevant authorities. Your employer can request you to write a report stating what transpired or the cause of the injury. Ensure that you have the details ready to simplify the claims process.

Employers also have a responsibility to guide you through the worker compensation process. They must outline the benefits attached to the policy that the insurer should fulfill in your contract.

2. Seek Medical Assistance

If the injury sustained is severe, seeking medical assistance should be a top priority. It enables medical practitioners to assess the extent of your injuries and give or recommend medical care for quick recovery.

The doctors will also question how the injury occurred to write a report for their records. It’s an administrative procedure that cannot be overlooked and may contribute to your claims case against your workplace or employer.

3. Get A Doctors’ Report And Certificate

Doctors must issue a certificate stating their diagnosis of your work-related injury. It’s a supporting document that you can use in your compensation claims. The information can entail the cause of injury at the workplace and a rehabilitation program through medical care. It also captures what tasks at work you can handle while continuing to nurse your wounds.

4. Share the Report With Your Insurer

Your insurer needs to know that you suffered an injury at work early. So, it’s prudent to present a certified copy of your medical report and certificate of capacity for their records. Also, share the information with your employer to ensure that the relevant parties know your intentions to pursue worker compensation claims. It’ll help them to prepare for your file and any underlying process to fulfill their cover promises.

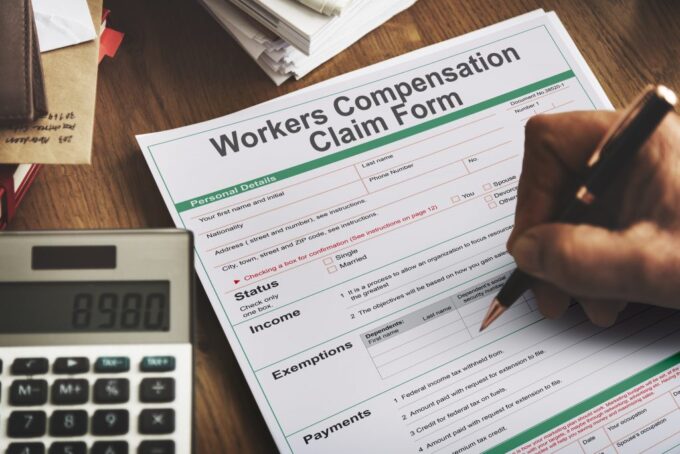

5. Fill out The Compensation Claims Form

There are a few paperwork requirements to launching a worker compensation claim. Your employer can provide as required by the insurance, or you can access the forms online platforms of your insurer.

It’s good practice to fill out the form according to the injury you sustained at the workplace. So, give precise details of the account that led to you getting hurt to help the insurer to settle the matter quickly. Also, it’s worth noting that the compensation claims form varies from state to state and the insurance providers you’ve enlisted.

6. Be Available For Investigations

Insurance providers must investigate the worker compensation claims presented by policyholders. It’s one way they countercheck the evidence presented to support your case. The insurer might want to visit the accident scene or review the authenticity of your doctor’s report and certificates. So, it’s crucial to avail yourself whenever the investigators request you to meet them.

You can carry photos and scans of your injury to show your medical care history. It’s additional weight to the evidence needed to recover claims from the insurer. In addition, being present can also be an opportunity for doctors to check if the rehabilitation works.

7. Establish A Return To Work Procedure

A return-to-work program does not necessarily involve getting financial benefits from your employer. It enables you to safely integrate into the working environment by considering the workload you can handle.

The insurance company might have to pay disability benefits for the injury you sustained at work. In that connection, your employer must adjust the tasks assigned to you or invest in training and developing your skills to continue working for them. However, it would be best if you had it in writing to notify your employer and the insurer of your intended resumption to duty.

8. Have A Lawyer To Countercheck

Workers’ compensation claims can be hard to crack if you disagree with the insurance law. You’ll end up frustrated by the insurance company’s back-and-forth requests and misinterpreting the policy clauses. Information gaps might take you longer to process and settle the matter with the insurer due to information gaps.

In such instances, consulting a lawyer can ensure you leave no stone unturned and settle the matter faster. You’ll follow through with laid down instructions and produce the evidence needed to support the claims submissions.

Final Thoughts

Injury at work should not be ignored due to the long-term effects on your health. You might spend time and money on future medical care that you would use to enjoy life. It’s crucial to learn what steps to take should you get hurt while on duty, the benefits attached to your insurance coverage, and the time limits on claims submitted to the insurance company. In addition, the insurance law needs a legal practitioner to explain the clauses cited in the policy and advice the best approach to your claims submissions.